Beef Burgers Inc Contracts to Buy Five Hundred

Colleen Michaels/iStock Editorial via Getty Images

Investment Thesis

Red Robin Gourmet Burgers' (NASDAQ:RRGB) performance is improving, albeit slowly. Contributions from Donatos partnership should benefit the company. The company's revenue grew 21% year over year in the latest quarter, while it generated positive income from operations. The stock's price should recover with improved operational and financial performance of the company.

However, with operations-level losses dating back to 2018, it might be better to wait and watch the company's progress before buying the stock.

Business

Red Robin Gourmet Burgers, Inc., operates casual dining restaurants in the U.S. As of December 2021, it had total of 531 Red Robin restaurants. Of these, 430 were company-owned and 101 were operated by franchisees. The company has a presence in 44 states along with one Canadian province.

Burgers accounted for nearly 58% of the food sales in 2021. Apart from that, the restaurant also serves a variety of Donatos pizza, wings, salads, other entrees, and desserts. The restaurants also serve milkshakes, signature alcoholic and non-alcoholic specialty drinks, cocktails, wine, and a range of national and craft beers.

Financials

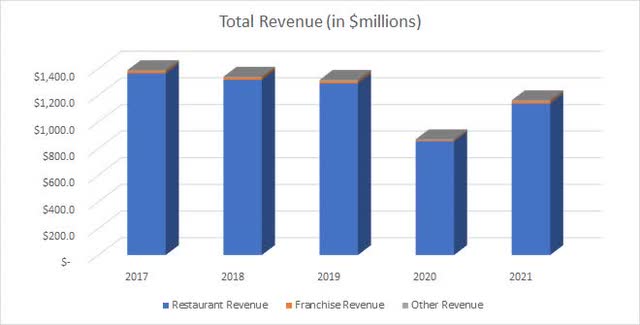

Sale of food and beverages at company-owned restaurants is Red Robin's primary source of revenue. Apart from that, the company also earns royalties and fees from franchised restaurants.

From 2022 to 2021, total revenue decreased at a rate of 4.3% CAGR. The trend in various revenue streams is seen in the chart below.

Red Robin Gourmet Burgers

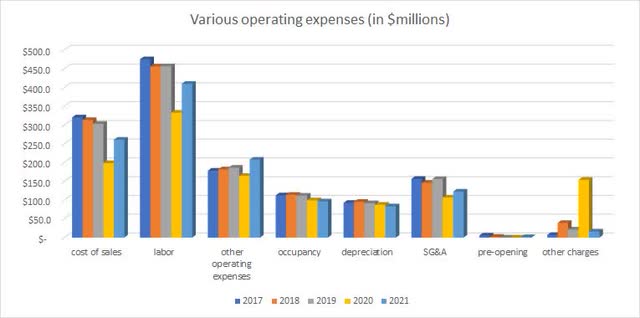

Labor and raw materials are the major operating costs for Red Robin.

Red Robin Gourmet Burgers

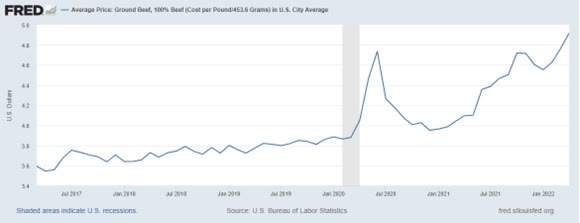

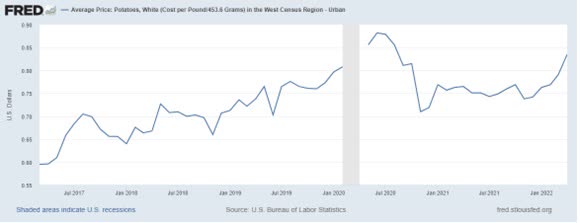

Of the total cost of goods in 2021, ground beef (16%), potatoes (12%), and poultry (11%) are the major components. Ground beef and potato prices have shown steady increase in the last five years.

U.S. Bureau of Labor Statistics

U.S. Bureau of Labor Statistics

The company has not been operationally profitable for four years consecutively.

Red Robin Gourmet Burgers

However, in the latest quarter, the company generated positive income from operations of $4.4 million, even though its restaurant-level margins got hurt by mainly food and labor cost inflation. What's more, the company expects that its restaurant-level operating profit margins will improve to 2022 level in 2023. It however expects higher commodity cost inflation of low double digits in 2022.

Long-term comparable restaurant revenue trend is also not very encouraging with negative growth in three out of five years. The increase in 2022 was a result of a lower base seen in the previous year due to the COVID-19 pandemic.

Red Robin Gourmet Burgers

However, in the latest quarter, comparable restaurant revenue increased 19.7% compared to 2021. Overall, though slowly, Red Robin's financials seem to be improving.

Partnership with Donatos

Red Robin entered a partnership with Donatos in 2020. As per the arrangement, Red Robin restaurants will prepare and serve Donatos branded pizzas. In exchange, Red Robin has agreed to pay royalties to Donatos pizza. By December 2021, the company introduced Donatos pizzas in its 198 restaurants. Management plans to introduce it into around 50 new restaurants in 2022 and expects to complete rollout in approximately 150 in 2023.

In the first quarter call, Paul Murphy, Red Robin Gourmet Burgers' CEO, noted,

Donatos Pizza sales reached more than $7 million in Q1 and were supported by additional marketing support at certain locations. Restaurant serving Donatos continue to outperform the rest of the Red Robin system. For restaurants that had Donatos, comparable restaurant revenue grew by more than 5% over restaurants that did not yet have Donatos.

Additionally, guest checks have included the Donatos Pizza were on average over $10 higher than those that did not include pizza. We also see that Donatos drives higher visit frequency among our loyalty members, adding one more visit per year.

Risks

- Fixed-price purchase commitments - To control its costs, the company enters fixed-price purchase commitments for certain commodities. As of December 2021, roughly 65% of the annual food and beverage purchases of the restaurant were covered under such contracts. Many of them are scheduled to expire during 2022. Expiring contracts with food suppliers could result in unfavorable renewal terms and may result in cost increases. This might affect the operating results negatively.

- Concentration risk - 170 out of a total 430 company-owned restaurants, contributing nearly 48% of the restaurant revenue, are in the western United States. This makes them susceptible to changes in economic conditions and other trends in that region.

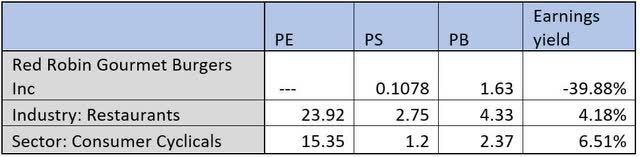

Valuation

Red Robin Gourmet Burgers

Red Robin stock is trading at a discount to industry based on Price to Sales and Price to Book Value ratios. The discounted valuation obviously reflects the fact that the company is incurring losses.

Seeking Alpha's proprietary Quant Ratings rate Red Robin stock as "sell." The stock is rated low on profitability, momentum, and revisions factors. The rating should improve, as the company returns to profitability. Further, with the company beating revenue and earnings estimates in the latest quarter, analysts will likely revise their estimates upwards.

Conclusion

Donatos pizza is adding incremental revenue to Red Robin and should contribute to the company's progress towards profitability. Losses have narrowed, and Red Robin generated positive income from operations in the latest quarter.

On the flip side, the company incurred losses at the operations level starting from 2018, well before the pandemic. The chain has not been able to manage commodity price inflation and hasn't returned to profitability even though customers are returning to restaurants and most of the top restaurants have already returned to profitability. Nearly half of Red Robin's revenue comes from the western United States.

For the above reasons, despite the improvements, it might be too early to buy this stock right now.

This article was written by

We provide end-to-end financial research services across asset classes. We are passionate about stocks and investments. We take pride in providing invaluable investing insights in an easy-to-understand way. .Chandan Khandelwal leads RCK, as its co-founder & CEO. He is a Chartered Accountant and Financial Consultant with more than 15 years of experience in Finance, Stock Market, Assurance and Business Advisory.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Source: https://seekingalpha.com/article/4515064-red-robin-gourmet-burgers-posts-improved-q1-performance-but-is-it-good-enough

0 Response to "Beef Burgers Inc Contracts to Buy Five Hundred"

Post a Comment